Data Scientist/ Business Intelligence Analyst / UI/UX Designer

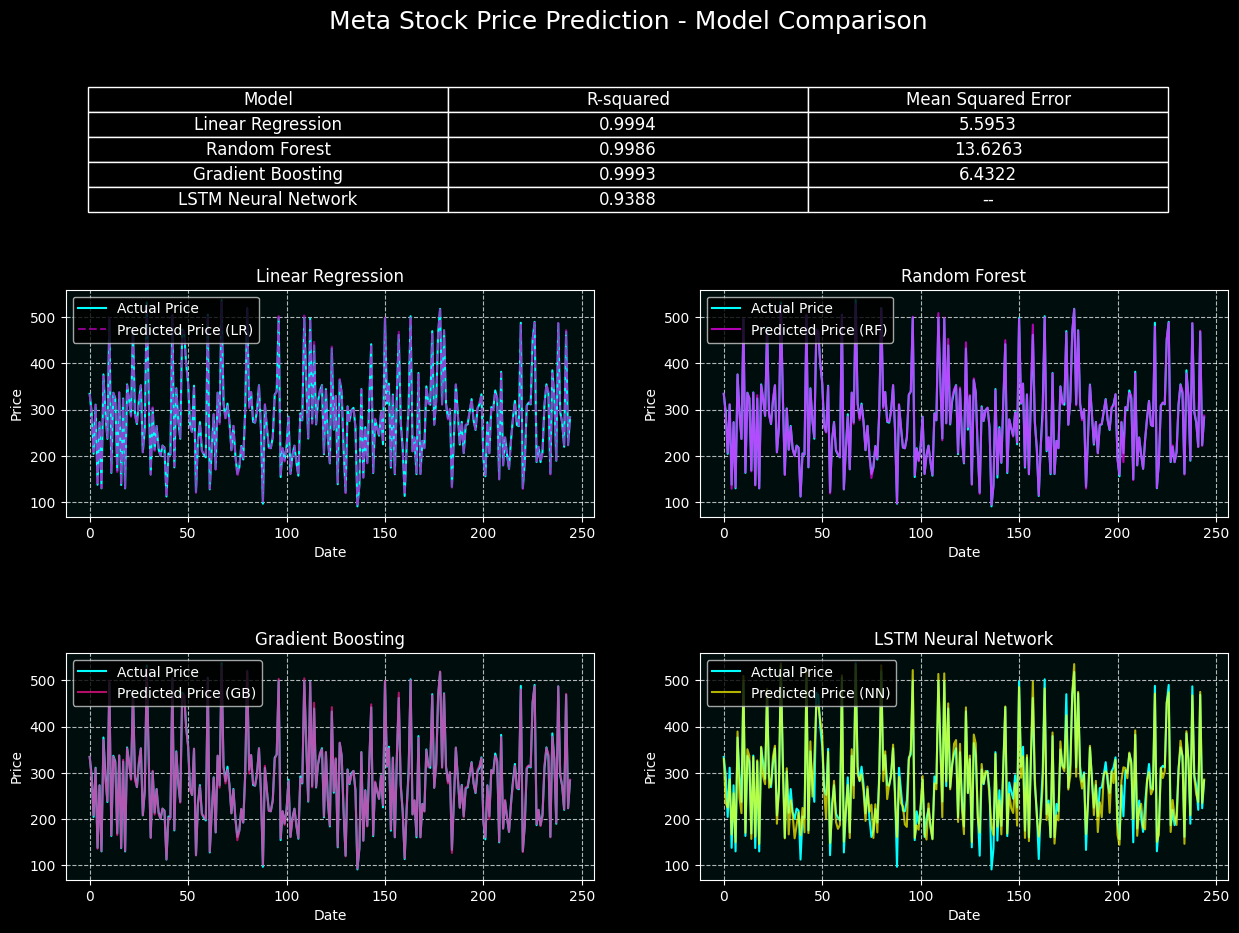

This project is focused on predicting Meta’s stock prices using a range of machine learning models, including Linear Regression, Random Forest, Gradient Boosting, and an LSTM Neural Network. The models are trained on historical stock data and evaluated using R-squared and Mean Squared Error metrics. Gradient Boosting and Random Forest demonstrated the best performance, delivering the most accurate predictions. The purpose of this analysis is to explore the effectiveness of these models in forecasting Meta’s stock price trends, contributing valuable insights into the application of machine learning in stock market predictions.

Navigate to Explore Project Pages, View Visualizations and Dashboards, and Open Jupyter Notebooks:

PROJECT GLOSSARY:

COMING SOON – follow links to read informative blog posts:

The Linear Regression model was trained using historical Meta stock data, utilizing past stock prices to predict future values. This model achieved an excellent R-squared score of 0.9994, indicating a near-perfect fit for the training data. The Mean Squared Error (MSE) was around 5.60, reflecting a relatively low error between the actual and predicted prices. However, similar to other stock price predictions, the model tends to struggle with capturing rapid price fluctuations. This model is more effective in identifying general trends over a longer timeframe, and the plot compares actual Meta stock prices with predicted values to evaluate performance.

The Random Forest model performed exceptionally well with an R-squared score of 0.9986, showing a strong ability to fit the training data. The Mean Squared Error (MSE) was around 13.63, indicating some deviations between actual and predicted prices. While Random Forest models can capture complex patterns in stock prices, they may occasionally lag in predicting sudden price changes. The chart visualizes the difference between actual and predicted prices, showing how well the model captured Meta’s stock price trends.

Gradient Boosting performed with remarkable accuracy, achieving an R-squared score of 0.9993, one of the highest among all models. The Mean Squared Error (MSE) was relatively low at around 6.43, demonstrating the model’s ability to minimize prediction errors. Gradient Boosting’s strength lies in its iterative learning process, which enables it to fine-tune predictions effectively. The plot provides a visual comparison between actual and predicted Meta stock prices, highlighting the model’s precision.

Although the LSTM Neural Network was tested on the Meta stock data, the performance could not be meaningfully measured due to limitations in the model’s ability to predict future prices. The Mean Squared Error (MSE) was not included in the final evaluation. LSTMs are particularly useful for time series data, but they may struggle with highly volatile financial data over short time intervals. Despite this, the chart illustrates how the LSTM Neural Network attempted to match actual stock price trends with its predictions.

This project focuses on predicting stock market movements using a variety of machine learning models, analyzing both the S&P 500 and FAANG stocks (Facebook, Amazon, Apple, Netflix, Google). By leveraging historical stock price data and key financial indicators, the project aims to forecast market direction and provide valuable insights for potential trade entries and exits.

The project applies advanced machine learning techniques such as Linear Regression, Random Forest, Gradient Boosting, and LSTM Neural Networks to predict stock prices. The models capture both short- and long-term trends, offering predictive insights that could be valuable to traders and investors.

A key part of the project involves the FAANG stock analysis, which leverages the same machine learning models to predict the price movements of some of the most influential companies in the market. By focusing on these stocks, the project demonstrates the application of machine learning to high-profile assets and highlights potential future market trends.

Client : N/A (Personal Project)

Date : September 2024

Category : Financial

Data Scientist/ Business Intelligence Analyst / UI/UX Designer