Data Scientist/ Business Intelligence Analyst / UI/UX Designer

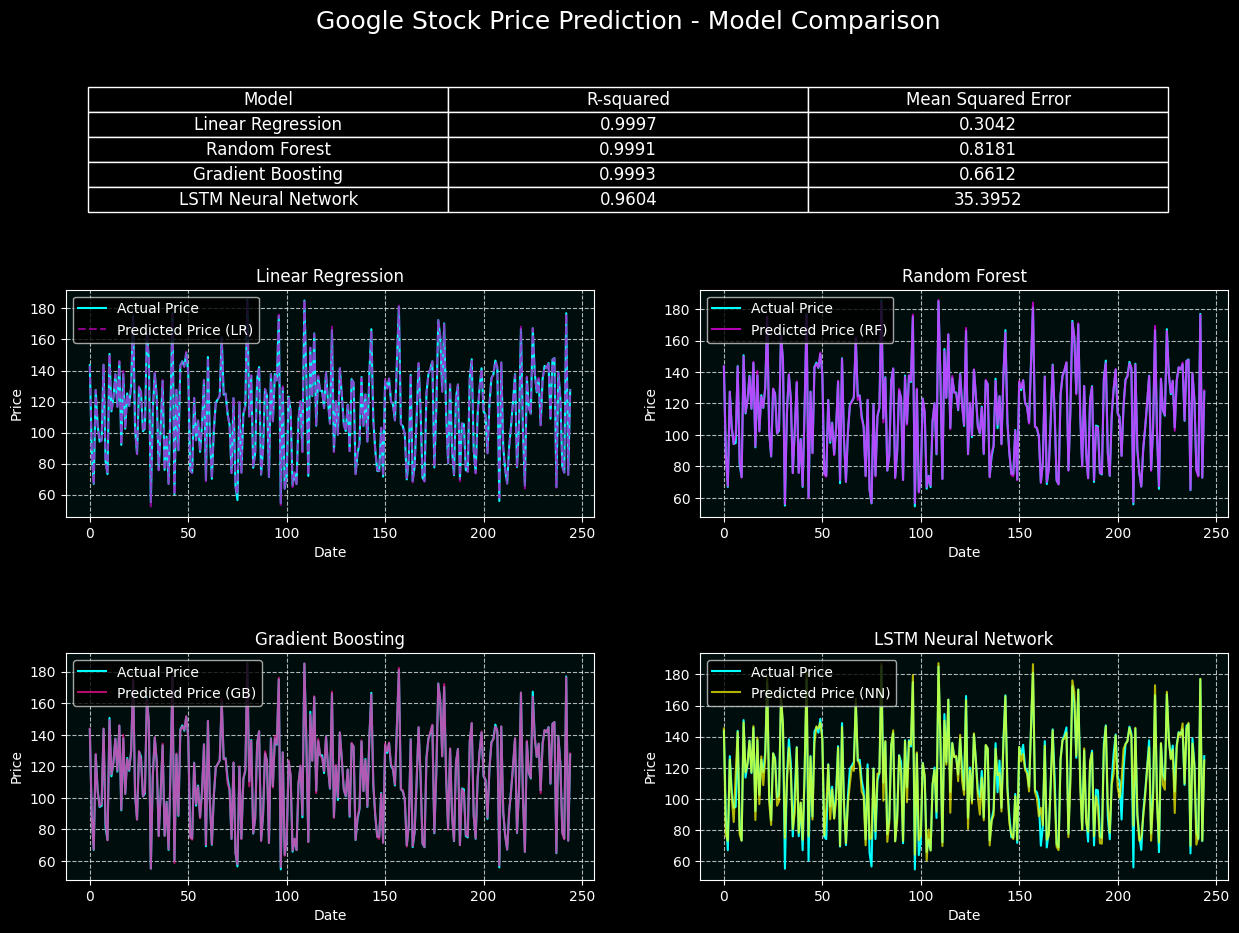

This project focuses on predicting Google’s stock prices using a variety of machine learning models, including Linear Regression, Random Forest, Gradient Boosting, and an LSTM Neural Network. The models are trained on historical stock data and evaluated using R-squared and Mean Squared Error metrics. Linear Regression and Gradient Boosting demonstrated the best performance, delivering highly accurate predictions. The purpose of this analysis is to assess the effectiveness of these models in forecasting Google’s stock price trends, offering valuable insights into applying machine learning to stock market predictions.

Navigate to Explore Project Pages, View Visualizations and Dashboards, and Open Jupyter Notebooks:

PROJECT GLOSSARY:

COMING SOON – follow links to read informative blog posts:

The Linear Regression model was trained using historical Google stock data, utilizing key features like past stock prices to predict future stock prices. The model achieved an impressive R-squared score of 0.9997, indicating an almost perfect fit for the training data. The Mean Squared Error (MSE) was around 0.3042, reflecting an exceptionally low error between the actual and predicted prices. This shows that the Linear Regression model effectively captures overall price trends but may not fully capture short-term volatility. The plot compares actual Google stock prices against predicted prices to visualize its performance.

The Random Forest model produced outstanding results with an R-squared score of 0.9991 and a Mean Squared Error (MSE) of 0.8181. This model performed exceptionally well in capturing the overall trend of Google stock prices, utilizing the ensemble of decision trees to reduce variance and improve prediction accuracy. It is more robust in handling noise in stock data and better at predicting stock prices during volatile periods compared to the Linear Regression model.

Gradient Boosting outperformed other models with an R-squared score of 0.9993 and a Mean Squared Error (MSE) of 0.6612, making it the most accurate model for predicting Google stock prices. By building models sequentially and minimizing prediction error, Gradient Boosting is particularly effective in capturing both long-term trends and short-term fluctuations in stock prices. The Gradient Boosting plot shows the close alignment between actual and predicted prices.

The LSTM Neural Network, designed to capture time-dependent patterns in stock prices, achieved an R-squared score of 0.9604 and a Mean Squared Error (MSE) of 35.3952. While it captured long-term trends well, the model struggled to maintain accuracy during periods of high volatility. Despite the lower performance compared to the other models, the LSTM still offers valuable insights into time-series forecasting and the potential of deep learning for stock prediction.

This project focuses on predicting stock market movements using a variety of machine learning models, analyzing both the S&P 500 and FAANG stocks (Facebook, Amazon, Apple, Netflix, Google). By leveraging historical stock price data and key financial indicators, the project aims to forecast market direction and provide valuable insights for potential trade entries and exits.

The project applies advanced machine learning techniques such as Linear Regression, Random Forest, Gradient Boosting, and LSTM Neural Networks to predict stock prices. The models capture both short- and long-term trends, offering predictive insights that could be valuable to traders and investors.

A key part of the project involves the FAANG stock analysis, which leverages the same machine learning models to predict the price movements of some of the most influential companies in the market. By focusing on these stocks, the project demonstrates the application of machine learning to high-profile assets and highlights potential future market trends.

Client : N/A (Personal Project)

Date : September 2024

Category : Financial

Data Scientist/ Business Intelligence Analyst / UI/UX Designer